Hi there. Today we’ll be discussing the ways in which contemporary cooperatives incentivize founders to take entrepreneurial risk and reward their visionary zeal within the cooperative structure. This question regularly arises in our work.

Let’s start by unpacking what founder equity is really all about. When an entrepreneur starts up a new business, they’re taking a huge risk. Putting it all on the line for an idea they believe in. Many times, founders toil away on nights and weekends to get the idea off the ground until the business has gained enough validation to leave one’s place of steady employment. Founding a company puts a HUGE toll on a founder, her or his family, finances and friendships. Founding a company is an act of courage and bravery. It’s not for the faint of heart.

So, to ensure that a founder stands to benefit from the fruits of her or his efforts, founders are often allocated a substantial, if not controlling, interest in the company. This ensures the founder can exercise control over the vision, key strategic direction and major decisions the company will face. Particularly when it comes to bringing on new capital and potentially diluting the founder with equity awards to other key stakeholders, carving out a majority interest is important to ensure the founder has control. Control in the sense of governance – running the Board and even controlling the company’s shares.

Also, allocating a majority of stock for the founder also ensures the founder reaps a commensurate reward for the company’s success when it comes to dividends and the proceeds of a profitable liquidity event. Founders often hold tightly their coveted controlling interest for fear that investors will oust them if times get tough, if investor returns are subordinated for a social purpose, or if the founder’s vision for operating the company diverges from that of the investors.

Enlightened founders realize what they really need to be successful is a talented team, aligned by a shared purpose. Shared purpose and values creates more incentive and motivation than any rising star shares ever could. After all, I have never heard of a founder who felt proud about the windfall they received when their company was forcibly sold at the peak of its economic value if the founder believed its social purpose had not fully been fulfilled.

Not all founders want to build a company to sell to the highest bidder. Many founders are looking to build generative companies that seek to contribute durable value to customers, communities, the environment and shareholders (see Zebra companies, B-Corps, Cooperatives). To found a company like this, many founders realize they need to build a stakeholder community with shared purpose and values.

***

Cooperatives, by design, dilute each and every member in terms of control and economic upside. Why? Members typically vote democratically, one-member, one-vote. Also, profits and liquidity proceeds are divided according to patronage.

Wait, what’s patronage again, you ask. A brief refresher. Patronage refers to the core business value a member contributes or consumes in relation to the total value of business the cooperative does with its members.

Traditionally, “pure form” or single class cooperatives organized themselves as either worker (W2 or contractor labor), producer (independent business producer), purchasing (independent business purchasing), or consumer (individual consumer for personal use) cooperatives. Not until the development the Uniform Limited Cooperative Association Act (“ULCAA”), and its adoption in 6 states around 2011 did the multi-stakeholder cooperative model take root. Today, most of our cooperative start-ups rely on the ULCAA statute in Colorado to structure multi-stakeholder cooperatives, known as limited cooperative associations (“LCA”). The emergence of the multi-stakeholder LCA will be relevant to the question at hand.

***

Back to the topic at hand. So, if “economic incentive” is shared not on the basis of stock ownership, like a traditional corporation, but rather on the basis of patronage, then what incentive does a founder have to sweat for their equity? Also, if a founder has the same voting rights (remember, one-member, one-vote) as all other members, why would a founder want to give up that much control before the start-up is even off the ground?

For the sake of this blog, we’ll assume that the cooperative model and business structure makes sense to you as a democratically controlled, responsibly capitalized and equitably incentivized form of business. Also, we’ll assume that you’re moved by adopting a business structure that subscribes to and incorporates into its DNA the 7 cooperative principles.

There are 7 primary complementary mechanisms that contemporary cooperatives use to provide the expectant incentive for a founder to apply the same energy to a start-up cooperative as they would to a traditional corporation. These are listed in no particular order of prevalence or effectiveness.

1. Ownership: Founder Patron-Member Class.

Among the most exciting and interesting developments in the cooperative sector is the increasing use of the “multi-stakeholder” cooperative, that is a cooperative with multiple classes of ownership.

Founders can be recognized and conferred a bundle of ownership rights in their own class. Founders “patronage” can be recognized from the time of conception. The Founder class can be allocated an identifiable percentage of net profit as part of the cooperative’s patronage dividend allocation.

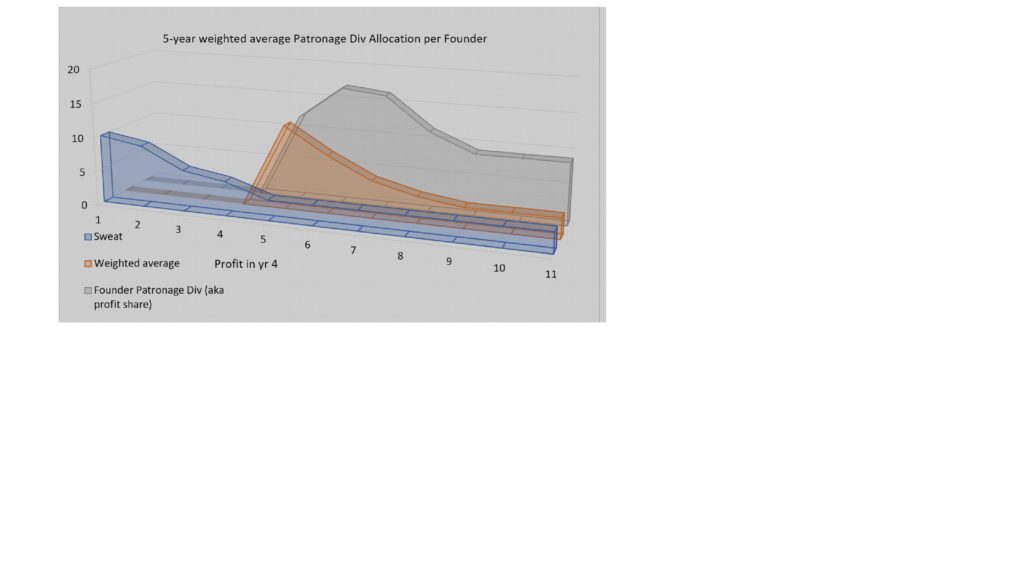

Individual Founder-member patronage can be difficult to measure. A few recent ideas have been gaining traction. Since Founders are often giving most of their time and energy to the enterprise before it can reasonably be expected to generate a profit, the “patronage dividend” may be a misaligned tool to incent or reward “sweat equity.” A founder’s hardest work would be rewarded by the expected early losses that most start-ups experience. That’s certainly not the fair result we’re after.

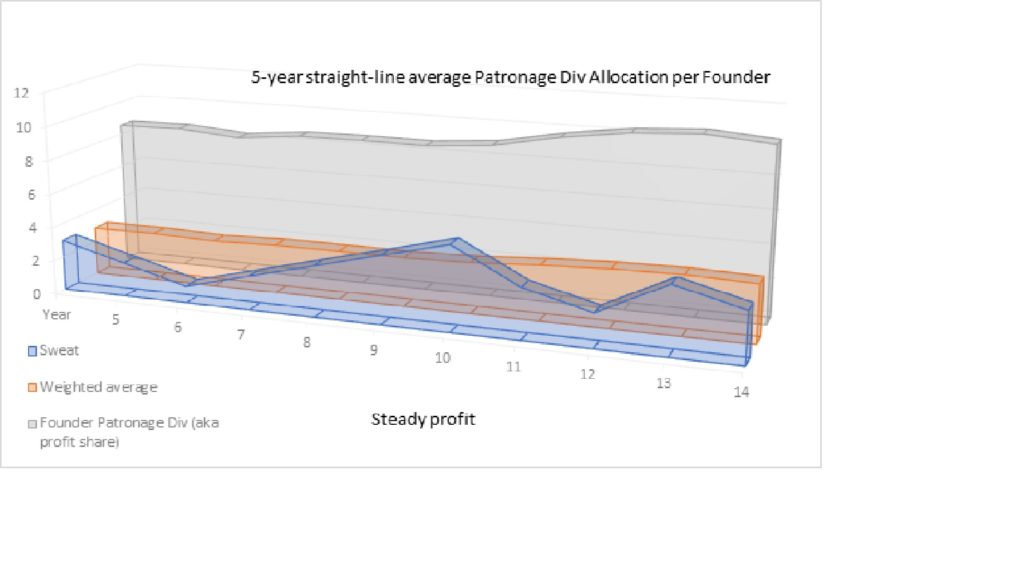

So, to “save up” that sweat equity and apply it to periods when the cooperative is or should be profitable, the Founder-member class can adopt a patronage allocation formula that takes a weighted average of the past X years, such that the early years of heavy sweat equity investment are weighted higher than later years.

The purpose of adopting a weighted-average formula is to recognize the early years when allocating the Founder-member patronage dividend. Perhaps once the cooperative is up and running, the weighted-average formula can be modified to just a straight-line average of X years.

2. Governance: Class based director seats with class-based director elections.

It is common for the Board of Directors of a multi-stakeholder cooperative to allocate Board seats among the various ownership classes. Since most Boards must have a majority of seats filled by “patron-members,” bylaws could certainly provide for board seats to be filled by a certain number of founders.

In fact, whether or not the cooperative has created a distinct Founder-member class, the bylaws could either:

- Maintain a qualification requirement that a certain number of directors be among the founders; or

- Designate a share of Board seats to be filled by Founder-members. In this case, the number of Founder-member designated board seats could even represent a disproportionate share of the board in relation to Founder-members proportionate share of the membership writ large. As long as Founder-members constitute patron-members, there should be no problem creating a board with disproportionate Founder-member directors. Of course, the composition of the Board can be recalibrated over time either prescriptively in the bylaws or in an organic fashion by amending the bylaws (whether through a Board or member vote).

- Of course, the bylaws could also require that a certain number of the Founder-member directors need to be present to constitute a quorum of the Board. This ensures that no Board business can take place without Founder-member directors present.

While not necessary, it is becoming customary for class-based board seats to be elected on a “district” or class basis. That is, Founder-members would elect the Founder-member board seats separately from Class X members electing those certain Class X board seats.

3. Governance: Founder as initial director with reasonable runway prior to first director election.

Many cooperatives are formed with initial directors who serve until either a date certain or a member election to elect directors. Many times, founders or Founding-members serve as the initial directors of a cooperative. Depending on the applicable cooperative statute, the Cooperative may be permitted in its bylaws to defer a member election for a reasonable period of time to provide a runway for the initial directors. Initial directors are subject to the same pressures and forces that face traditional start-up founders. There is the pressure to develop an initial product or service, to achieve product-market fit, to finance early operations, and to recruit a top-notch team.

These challenges are compounded by the need of a cooperative to attract members, raise member capital contributions, and to develop and practice economic democracy.

Giving initial directors a reasonable runway before they’re subjected to the whims of a democratic election protects the early risk and effort required to get a start-up off the ground. It also sets expectations among members that outcomes and profitability are to be judged over the long-term, not based on quarterly results.

If initial directors were to have a few insulated years in leadership positions, it is more likely the first election will product elected directors on merit, and not based on restlessness.

4. Governance: Founder-Member quorum and member voting.

If the Cooperative maintains a Founder-member class, the bylaws could require a certain minimum number of Founder-members to be present at a member meeting to constitute quorum for the conduct of member business.

Taking this concept further, the bylaws could also require that if a vote is to be taken by Patron-members voting together on a one-member one-vote basis, that Founder-member approval as a separate class is also required. This could look like:

Quorum

- Lesser of 50 or 10% of All Patron-Members (Workers, Users, Founders) PLUS

- 2 Founder-Members

THEN

Voting

- Majority of Patron-Members voting together as a single class (Workers, Users, Founders) PLUS

- Super-majority of Founder-Members, voting separately as a class. Note: Does not include investor-member

5. Economics: Multiplier on Founder patronage vis-à-vis other patron-member classes.

If creating a Founder-member class does not make sense for one reason or another, an alternative approach could be to apply a multiplier to Founder’s time/contribution vis-à-vis other worker-members. This would weight Founder contributions when calculating patronage.

Given the problem identified earlier, this approach may only compound the inequity of applying a disproportionate share of early losses to the Founders. What we are trying to achieve is a financial interest in profit years after Founders took early risk and invested tremendous early energy (presumably with little or no guaranteed compensation).

6. Economics: Award preferred investor-membership interest/stock (either same or separate class as investor-members).

If a cooperative has created a class of stock to be sold to investors, the Cooperative could reserve a certain number of those shares to be awarded or sold at a discount to Founders. The Cooperative could either create a separate class or series of investor-shares to award to Founder-members, or it could award its single class of investor-shares to Founder-members.

Utilizing whatever economic rights to which the investor shares are entitled, awarding investor shares to Founders may offer a mechanism to offer modest economic upside.

Commonly, cooperative investor shares pay a target dividend, or make distributions up to an aggregate cap tied to the original purchase price. In both cases, the return on investment would provide some “equity-like” return for a Founder’s “sweat equity.”

Note that awarding stock that has a face value or fair market value higher than the award or purchase price may trigger an adverse tax consequence.

Subject to the requirements of the applicable cooperative statute and subject to the requirements of Internal Revenue Code sub-chapter T or sub-chapter K, respectively, the investor-shares awarded or sold at a discount to a Founder-member could be subject to appreciation. While it is most common for shares of a cooperative’s stock to be redeemable at the original purchase price, it is possible, with exceptions, to structure the investor stock so that the redemption price is higher than the original issue price. Of course, the mechanism by which the investor-shares are priced should be clearly expressed in the investment or award documents and approved by the Board. The Articles and/or Bylaws may also need to be amended to reflect the terms.

7. Founder as CEO with employment agreement approved by disinterested directors.

Most founders serve as their start-up’s first CEO. Among the connotations of the CEO title is the technical executive officer function to be played. That is, the CEO is often a functional management position appointed by and serving at the pleasure of the Board. Most boards don’t “do” the day-to-day work of the business; they hire and supervise a CEO.

Just like conventional start-ups, cooperative Boards can and often should appoint the founder to serve as the CEO. In fact, I often urge CEO appointments to be formalized with a written employment or services agreement that sets forth expectations, compensation (deferred, equity or otherwise), benefits, authority and termination. This is also the device by which the entity acquires right to the CEO’s intellectual property and business opportunities.

The written agreement is less about placing restrictions on the CEO, and more about establishing a framework for expectation setting and for delivering on an equitable exchange of value. Part of this exchange should involve a negotiation regarding compensation. Compensation can include salary, stock, deferred compensation, benefits, and even performance based pay. Note that there can be significant tax consequences to certain types of compensation and readers should always consult counsel and a tax advisor.

It is almost always advisable for these types of arrangements to be memorialized in writing. The cooperative should ensure that a sufficient number of independent directors ratify the agreement to avoid perceptions of impropriety or allegations of self-dealing.

***

Here is a presentation I was a part of covering the topic of founder compensation inside of cooperatives.